Picture supply: Getty Photographs

The Rolls-Royce (LSE:RR.) share worth has been the standout performer amongst FTSE 100 shares over the previous two years, rising practically 400%. What a outstanding turnaround it’s been since Covid-19 practically destroyed the enterprise.

So, what elements underpin the aerospace and defence inventory’s unbelievable efficiency? And might the expansion trajectory proceed?

Right here’s what the charts say!

Increasing margins

CEO Tufan Erginbilgiç’s tenure has been characterised by strategic initiatives and a price effectivity drive. Quickly after taking the job initially of 2023, he derided the agency as a “burning platform” that was underperforming opponents.

Since these feedback, the corporate’s undergone successive rounds of job cuts and adopted a extra streamlined enterprise mannequin. These adjustments have paid off handsomely.

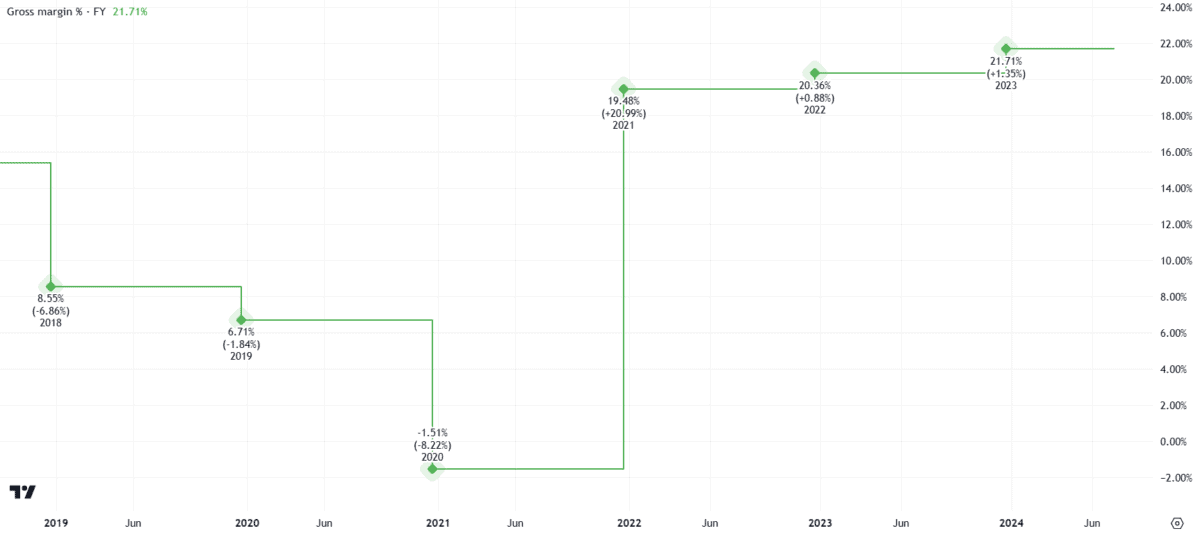

Rolls-Royce’s underlying working margin greater than doubled in FY23 to 10.3%. Furthermore, the gross margin of 21.7% is at a five-year excessive.

These figures are a window into the monetary well being of the enterprise, with implications for pricing methods, effectivity, and development potential.

There’s little doubt a powerful margins restoration has been a big issue within the Rolls-Royce share worth surge.

Debt discount

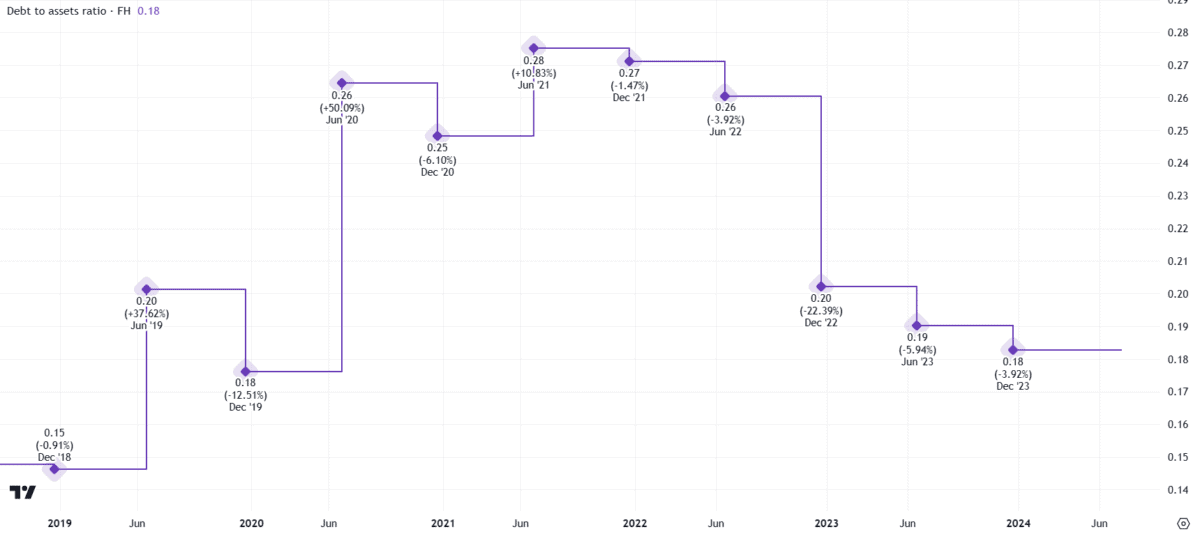

So too has the substantial stability sheet enchancment.

For context, Rolls-Royce was pressured to lift £7.3bn in debt and fairness on the top of the pandemic. Right now, the enterprise was burning by way of money to remain afloat whereas plane fleets remained grounded.

The outlook’s modified dramatically. Rolls-Royce has regained an investment-grade credit standing from all main companies. Web debt’s fallen to £2bn, down from £3.3bn on the finish of FY22.

Crucially, the debt-to-assets ratio has plummeted to simply 0.18. Consequently, the stability sheet seems to be significantly more healthy right now.

Valuation

Nevertheless, the corporate now has the next valuation.

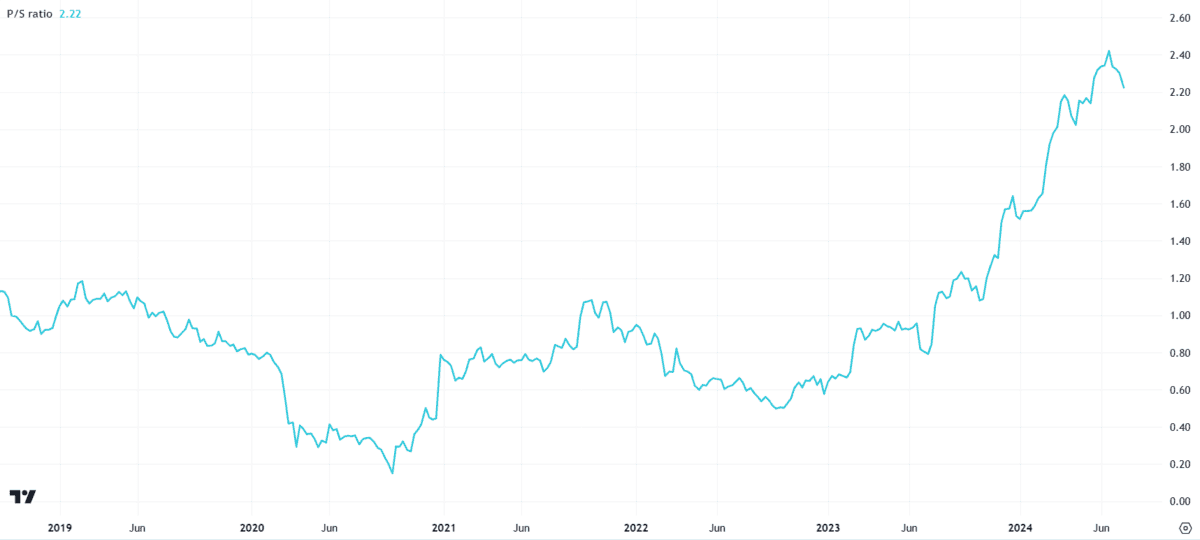

Historically, a price-to-sales (P/S) ratio between one and two is fascinating from an investor’s perspective. For Rolls-Royce, that a number of’s now eclipsed this higher restrict. The P/S ratio is at the moment 2.22.

This implies the Rolls-Royce share worth is not the discount it was in the course of the pandemic. A better valuation poses dangers to future returns.

I wouldn’t be stunned if the corporate’s inventory market efficiency over the approaching years isn’t as stellar because it’s been in recent times.

Rolls-Royce shares may have additional room to run if future earnings are good, however they’re in all probability nearer to being pretty valued than undervalued right now.

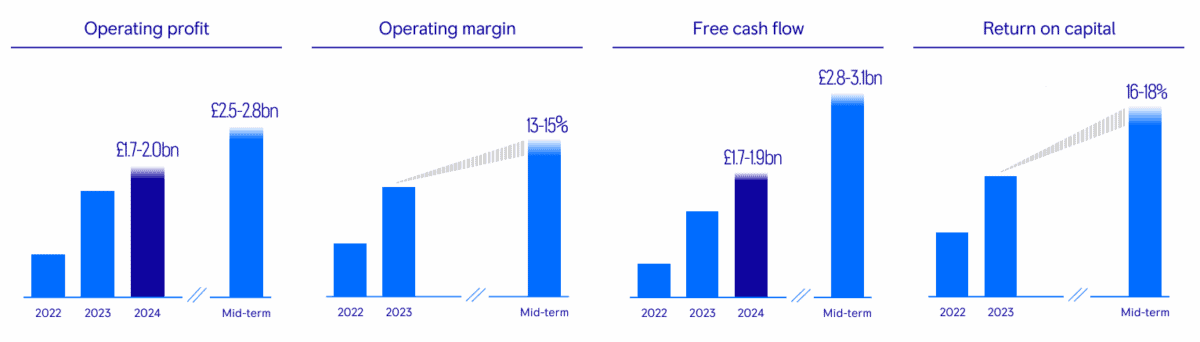

Future targets

Nonetheless, Erginbilgiç doesn’t lack ambition. Mid-term targets spanning a variety of metrics counsel there’s potential for additional enhancements according to a 2027 timeframe.

The group’s indicated these advances might be “progressive, however not essentially linear“. Accordingly, buyers ought to anticipate share worth volatility alongside the best way.

However, the large image’s broadly encouraging. The Civil Aerospace division ought to proceed to learn from an ongoing restoration in giant engine flying hours. Plus, the Defence arm has a number of potential development alternatives, such because the deployment of micro-reactor nuclear applied sciences in submarine fleets.

On stability, I feel the Rolls-Royce share worth development story stays intact, however we’ve in all probability seen the lion’s share of the beneficial properties already. I’ll proceed to carry my shares for now.

Buyers who’re eager to enter a place may take into account pound-cost averaging their share purchases to capitalise on any potential dips over the approaching quarters.

![Just released: Share Advisor's latest lower-risk, higher-yield recommendation [PREMIUM PICKS]](https://getmoneyskills.net/wp-content/uploads/2024/04/Just-released-Share-Advisors-latest-lower-risk-higher-yield-recommendation-PREMIUM-PICKS-150x150.jpg)